With gold prices near all-time highs, selling your gold can net you hundreds or even thousands of dollars. But do you get to keep it all? Everyone fears the tax man – and the regulations man for that matter – so let’s take a look at the implications of selling gold.

Like any other asset you might sell, from stocks and baseball cards to homes, if you sold it for more than you purchased it for, then you’ll likely be subject to capital gains tax. Capital gains tax is a tax on the profit made from the sale of an asset, and it applies to the difference between the purchase price and the sale price of the asset.

So, these rules don’t apply just to gold. If you sold silver, platinum or some other collectible to us (or another precious metals dealer), then you would be subject to capital gains tax.

And before we get too far, we should say that we aren’t tax and accounting professionals, and that tax codes can vary based on location and frequently change. It’s always advised to check with a local tax professional when preparing taxes or making large sales of your investments to make sure you follow the rules.

When it comes to income taxes, the IRS considers the sale of physical gold and silver a “collectible”. That’s bad news for taxpayers. It means rather than paying the typical capital gains rate, you’ll pay a maximum of 28%. If you’re in a lower income bracket, you’ll pay your normal rate. In other words, you’ll pay just like a short-term capital gains transaction, except the maximum tax rate is capped at 28%.

So for most people that are selling gold to us or someone else, this rule is going to apply. So, if you bought an ounce of gold when it was $500/oz and sold it for $2000/oz, the $1500 profit would be taxable at the rate of your income. If you’re a high earner (about $182k for someone single, $364k for a married couple), you’ll pay the 28% maximum, which in this case would be $420. So definitely make sure you set that aside or you’ll be surprised with a tax bill!

If you sell gold at a profit, it may be subject to capital gains tax. Capital gains tax is applicable when you sell an asset, such as gold, for more than you paid for it. In short, you’ll be paying tax on the profit from the transaction.

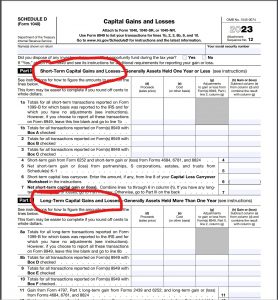

Long-Term Capital Gains Tax: If you held the gold for more than one year, the gain is typically considered a long-term capital gain and for most assets is subject to lower taxes. BUT NOT FOR PHYSICAL METAL SALES! This is due to the collectible status we covered above. So you won’t be reporting your gold sales in the long-term capital gains tax area.

Short-Term Capital Gains Tax: If you held the gold for one year or less before selling it, any profit is generally considered a short-term capital gain and is taxed at your ordinary income tax rate. Sales of collectibles (like gold and other metals, gems, and coins) are also taxed at this short-term capital gains rate. Here are the 2023 tax brackets on the IRS website. In this case, anyone earning over $10,276/year will pay some kind of tax for the sale. Most people are in the 22% or 24% tax brackets, so plan accordingly. If you’re paying a 22% tax, that would mean $330 in federal income tax.

Capital Gains tax is reported on Schedule D of Form 1040. Note how short- and long-term capital gains have separate sections. Collectible sales will all be reported in the short-term capital gains tax area.

The IRS considers scrap gold and jewelry a collectible as well. It still is taxed as the collectible rate.

Want to figure out how much you can sell your scrap gold for? See how to calculate the value of your scrap gold here!

Unfortunately, no, not really.

Physically-Backed ETFs: ETFs that are backed by physical gold are the same as owning the gold for tax purposes. So these ETFs are taxed like collectibles, rather than securities. That includes the popular $GLD ETF.

Correlated ETFs: Some securities tie closely to gold prices, such as gold miners and gold miner ETFs. Because these aren’t backed by the precious metals themselves, they are considered securities for taxation purposes. That said, investing in companies like this is far from the same as investing in gold itself. Many other factors come into play that affect their prices, although they do tend to correlate with the general movement of gold prices.

You may be wondering if you sell gold for cash to us, or a pawn shop, if the IRS will have any way to track the transaction to get their taxes from you. You probably weren’t wondering that because you’re an honest taxpayer (right? RIGHT?), but just so you know, transactions generally aren’t reported unless:

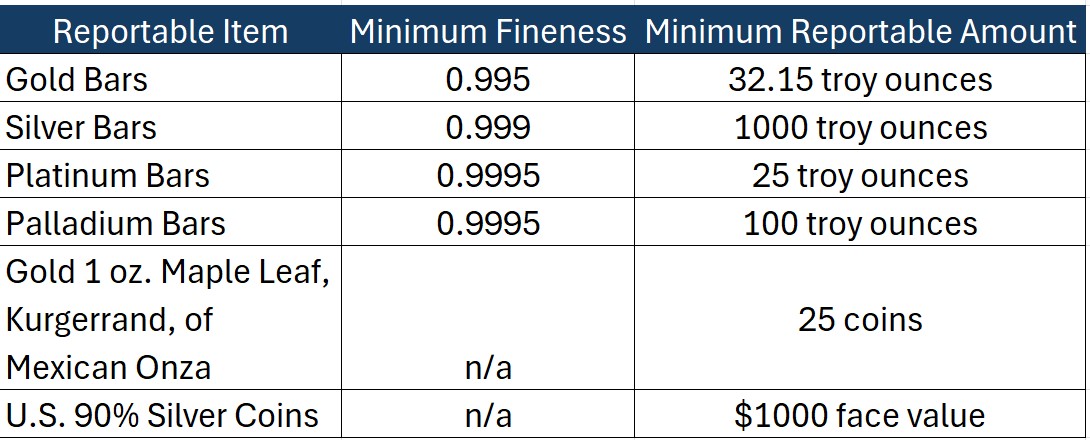

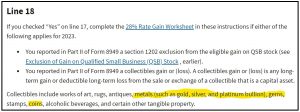

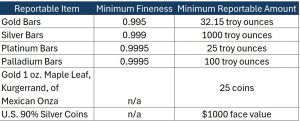

In addition, the The Industry Council for Tangible Assets (ICTA) negotiated with the IRS on reporting for form 1099-B, which established the following rules for reportable transactions.

Note that it’s just for proper coins and bullions, not for scrap gold. But even then, the minimum reporting requirements here amount to a large quantity. At over $2k/ounce, 25 coins are worth 50k. 32 bars would result in a sale of over $64k. The lowest amount would probably be selling a large quantity of common silver coins. With dimes going for about 17x their face value, you’re still looking at a transaction size over $15k. So in short, unless you’re selling a lot of gold and silver bullion, it’s unlikely that the company you’re selling to will be filing a 1099-B.

If you’re selling gold – whether it’s scrap gold jewelry or gold bars – most people will be taxed on the profits of the transaction at their normal income tax rate. Report it on form 1099, Schedule D, with the rest of your capital gains transaction.

And of course, ask your accountant if there is anything else to consider and get expert advice if you’re unsure of what to do.

POSTED IN: Capital Gains Tax, Gold Sale Reporting, Taxes on Gold, The IRS and Gold

By submitting your information you agree to our

Privacy

Policy and Terms and Conditions.